lands on 10-day IL")

Andrii Yalanskyi/iStock by way of Getty Pictures

Greater than meets the attention: Sturdy valuations don’t imply low danger

Lately, my daughter and I had been snowboarding at Beaver Creek. We occurred to share a chairlift with an teacher on our first trip up. We’re each nonetheless novices, and from the carry the mountain regarded forgiving—clear skies, groomed snow, large runs. All the pieces appeared manageable. I informed Alina it regarded like day for 2 individuals who had extra confidence than capability to be out on the mountain.

As we rode up, the trainer identified issues we had missed. Snowfall had been restricted, leaving fewer runs open and pushing extra skiers onto the identical trails. The trainer cautiously detailed how site visitors was heavier than common, resulting in main backups and extreme collisions at key choke factors. In some areas, restricted snowfall left a skinny layer of snow that hid patches of ice beneath. Circumstances appeared benign, however accidents mounted—seemingly the results of the harmful mixture of widespread overconfidence coupled with these extra delicate hazards. None of this was apparent from me and Alina hovering above, however all of it issues as soon as you might be on the mountain. What struck me was how deceptive my preliminary learn had been. From a distance, circumstances regarded calm. Solely after listening extra rigorously did it turn out to be clear that the margin for error was narrower than it appeared.

That have captures one thing that feels true about fastened earnings markets right now.

Primary optics would lead most to conclude that circumstances are benign. Costs are steady, credit score spreads are close to traditionally tight ranges, refinancing appears to be like straightforward for many issuers, and valuations assume the street forward stays easy. Markets are usually not broadly pricing stress. For a lot of traders, that calm feels reassuring.

However robust valuations don’t imply low danger. As on the mountain, easy surfaces can conceal hazards that solely reveal themselves as soon as you might be in movement, and overconfidence born of seemingly benign circumstances can itself create incremental danger. In fastened earnings, the most expensive errors are likely to happen not when circumstances look troublesome, however after they look straightforward.

At Harris | Oakmark, value is danger

When markets are calm and costs are excessive, it’s tempting to consider that danger has diminished. Securities commerce easily. Refinancing appears to be like straightforward. Credit score spreads sit close to their tightest ranges. Little or no seems fallacious.

That’s normally once we decelerate.

In environments like this, alternative tends to be selective moderately than widespread. With spreads this tight, ahead returns are prone to come primarily from earnings if circumstances stay constructive, not from a repricing of danger. That isn’t a foul end result. It merely means traders are being paid to clip coupons, to not be heroes.

At Harris | Oakmark, we remind ourselves that value is danger. A safety bought on the proper value can take up dangerous information. The identical safety bought on the fallacious value can not. Easy pricing can create a false sense of security when valuations assume favorable outcomes. The hazard is just not volatility. It’s paying an excessive amount of for certainty.

For this reason we give attention to long run fundamentals. We give attention to how an issuer’s leverage is prone to evolve over time and its capability to fulfill curiosity and different fixed-charge obligations based mostly on our expectations for profitability. Importantly, we additionally give attention to draw back danger, as credit score is in the end priced on the likelihood of default or impairment. If our assumptions show fallacious because of company-specific components or broader financial shifts, we assess an issuer’s capability to fulfill its obligations even in intervals of stress—supported by adequate asset protection within the occasion of liquidity stress, and by money flows and capital buildings which might be versatile and resilient. These draw back dangers don’t disappear as a result of markets really feel comfy.

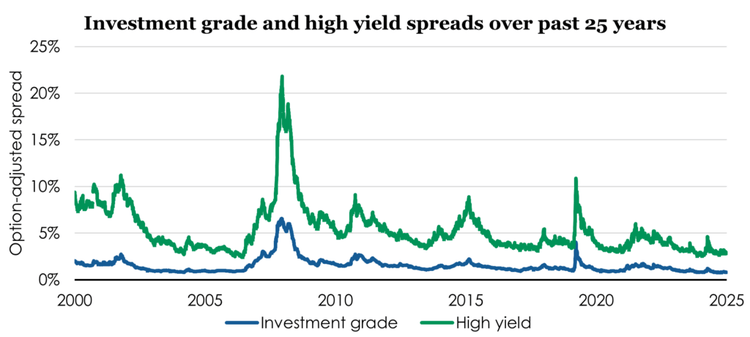

That distinction issues right now. As of year-end 2025, investment-grade company bonds yielded roughly 4.8 % with spreads close to 80 foundation factors over U.S. Treasuries. Excessive-yield bonds yielded about 6.5 % with spreads close to 290 foundation factors. Compensation for taking up company default danger sits close to the tight finish of historic ranges, whilst issuer leverage and different key credit score metrics have begun to melt modestly. Costs indicate confidence, however they depart little room for disappointment.

Information supply: Ice Information Indices, LLC, retrieved from FRED, Federal Reserve Financial institution of St. Louis, funding grade: ICE BofA US Company Index, excessive yield: ICE BofA US Excessive Yield Index, as of 12/31/25.

Additionally it is price noting what markets seem comfy overlooking. Geopolitical tensions have escalated throughout a number of areas, touching main vitality producers, commerce routes, and international political stability. We don’t try to predict how these conditions will resolve. However it’s troublesome to argue that they’re meaningfully mirrored in credit score pricing right now.

Though it looks like for much longer, lower than a yr in the past coverage headlines round tariffs—in the end extra negotiating posture than a willingness to disrupt the worldwide economic system with 100% plus tariffs—had been sufficient to push high-yield spreads roughly 60 % wider in a brief interval, with investment-grade spreads widening by roughly 55 %. At present, arguably extra consequential developments are producing little response in any respect. That distinction is price conserving in thoughts.

We’re additionally conscious of the rising position non-public credit score performs in right now’s market. In lots of circumstances, belongings that may have repriced extra rapidly in public markets during times of stress at the moment are held in buildings with completely different liquidity, valuation, and reporting dynamics. That doesn’t make these investments inherently dangerous. Nonetheless, it could sluggish the suggestions loop that market pricing sometimes offers and, in doing so, delay the popularity of underlying points. Whereas non-public credit score is just not but systemically necessary, for my part (primarily, due to dimension), it’s more and more intertwined with a lot of crucial issuers in main fastened earnings benchmarks. When suggestions is muted, value discovery tends to reach later—and extra abruptly.

We’re equally attentive to circumstances amongst decrease and middle-income customers. Early indicators of stress, together with larger delinquencies and slower compensation habits, emerged within the second half of final yr. These tendencies are usually not but decisive and extra not too long ago have really decelerated, however they warrant consideration in a market that seems to be pricing in little or no danger throughout a number of fastened earnings asset lessons.

Taken collectively, these observations don’t argue for wholesale warning; they argue for selectivity. At present, we’re discovering worth in choose areas of the non-agency securitization market and are more and more spending time evaluating alternatives in company credit score to probably add publicity in higher-quality however not too long ago pressured sectors equivalent to chemical compounds, know-how, healthcare, and others that we now have been traditionally underweight versus our friends and broader benchmarks.

Importantly, a few of the repricing in these areas is warranted, as fundamentals have deteriorated. The place we glance so as to add publicity is the place the market has overreacted—pushing costs too low or failing to offer adequate credit score to firms with the power to get better over time. Inside these sectors, there are additionally issuers the place the chance of additional elementary erosion is appropriately mirrored in valuations, which makes cautious safety choice important. Our focus is on figuring out firms which have been unduly penalized by broad sector sentiment moderately than by their very own fundamentals.

Danger is inherent in lending. The related query is whether or not we’re being adequately compensated for taking it.

That self-discipline additionally preserves flexibility. By not forcing investments when valuations are full, we preserve the power to behave when costs transfer sooner than fundamentals. That is typically most respected when it feels least obligatory. We acknowledge that this method is just not all the time comfy. In calm markets, self-discipline can really feel like inactivity. We settle for that discomfort. We might moderately danger trying early than be compelled to behave solely after costs modify.

Making ready for when circumstances change

Calm circumstances don’t remove cycles, they postpone the reminder that cycles exist. We had been reminded of this earlier in 2025. From April via June, tariff-related headlines triggered a fast shift in sentiment. Spreads widened, costs adjusted, and liquidity thinned. What stood out was how little fundamentals had modified. Stability sheets remained intact. Money flows had been steady. Structural protections held. Costs modified way over financial actuality.

As a result of Harris | Oakmark entered that interval conservatively positioned, we weren’t compelled to reply defensively. Valuations earlier within the yr had not justified leaning in. When costs dislocated and sentiment shifted, we had been capable of act. Over the primary 5 months of the yr, we added roughly twelve factors of credit score danger, deploying capital selectively the place costs moved greater than fundamentals.

That episode bolstered a easy lesson. Preparedness is a part of self-discipline. Ready is just not inactivity. It’s positioning. Durations of stress hardly ever announce themselves. They arrive rapidly and are amplified by investor psychology. After they do, the window to behave is commonly temporary. Being prepared issues greater than being early.

At present, valuations once more indicate confidence, and alternative is narrower. We’re conservatively positioned, as we had been firstly of final yr. That posture is intentional. We don’t attempt to predict when the following interval of stress will arrive. Markets have a protracted historical past of unusual traders. What we will management is readiness, the power to behave when feelings detach from fundamentals, and the persistence to attend when they don’t.

The mountain doesn’t announce when circumstances change. A path that appears straightforward from the carry can demand extra consideration midway down. Fastened earnings investing works the identical means. By staying disciplined when valuations are principally full and ready to behave when costs dislocate, at Harris | Oakmark, we search to handle danger intentionally and deploy capital when alternative is actual, not merely when it appears to be like comfy.

Adam D. Abbas, Portfolio Supervisor

Editor’s Be aware: The abstract bullets for this text had been chosen by In search of Alpha editors.