")

John Twohig/iStock through Getty Photographs

SBA Communications Company (NASDAQ:SBAC) is a number one proprietor and operator of wi-fi communication infrastructure. There was some information on the finish of August from AT&T (T) that despatched SBAC’s inventory value down. You possibly can learn that information right here on the AT&T web site. I’ll be breaking down the details of this story so buyers can have a greater image of what’s happening.

In brief, this wasn’t an enormous unfavorable for SBAC. Now let’s get into the lengthy reply.

Why is the FCC concerned?

Why was there an inquiry from the FCC? I consider it was as a result of EchoStar (SATS) was failing to deploy the bandwidth successfully. Firms bidding on the “rights” for bandwidth would not have the “proper” to squat on that bandwidth. It have to be deployed to learn the residents. Since SATS was not deploying it successfully sufficient (allegedly), they bought it to AT&T.

This got here up on the investor name as nicely. AT&T apparently paid about $7 billion extra to buy the spectrum than EchoStar paid once they bought it.

Value to AT&T: $23 billion.

Revenue to EchoStar: $7 billion.

EchoStar’s unique value: Implied $16 billion.

EchoStar Share Value

The next math makes use of an approximation of 287.8 million shares excellent.

Earlier than the deal, EchoStar was buying and selling round $29.62. Market cap of widespread fairness = $8.5 billion.

At the moment, EchoStar is buying and selling round $56.15. Market cap of widespread fairness = $16.2 billion.

Improve in EchoStar’s complete enterprise worth (fairness + debt) = About $7.7 billion.

On condition that EchoStar’s worth is up by about $7.7 billion following a revenue of $7 billion on the spectrum (needs to be pretax), we are able to fairly assume that EchoStar buyers had been valuing the spectrum someplace round $16 billion.

The Press Launch Plans

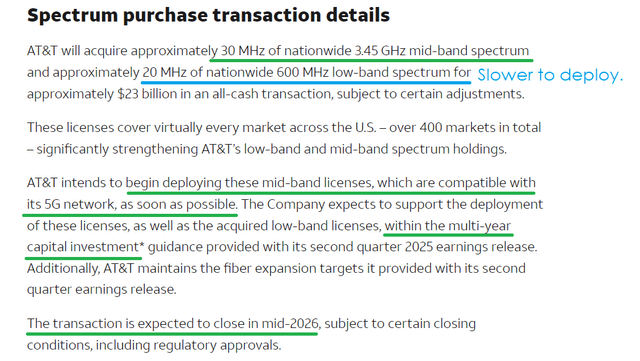

Within the press launch, AT&T emphasised that they might be deploying the three.45 GHz spectrum as rapidly as potential. There might be a modest delay in getting the 600 MHz spectrum energetic.

AT&T

That is smart as a result of the three.45 GHz suits very nicely with what AT&T is already utilizing. The 600 MHz spectrum would require some changes to tools. Administration says a few of their tools was nearing finish of life anyway, so upgrading the tools to additionally cowl that spectrum needs to be fairly environment friendly.

A Fast Observe: I’ll simply pause right here to notice that prior commentary from tower REIT executives signifies that putting in new tools to cowl extra spectrum requires amendments which enhance lease.

It seems like it is going to take a few years as AT&T deploys that 600 MHz spectrum. It’s fairly a little bit of spectrum requiring {hardware} changes, so it’s no shock that it might take time to do all of these upgrades.

The Income Case for AT&T

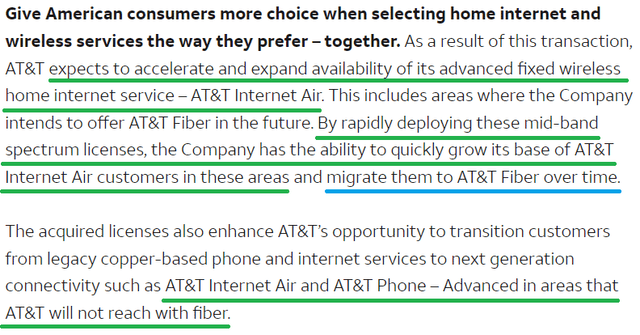

AT&T highlights this as a strategy to increase availability of fastened wi-fi residence web service:

AT&T

That’s not dangerous for the towers both. When AT&T Web Air features new prospects it places extra visitors on the airwaves. That’s higher than having that visitors operating over cable. Finally AT&T wish to transfer a few of these prospects over to fiber, however AT&T even acknowledges that many purchasers won’t ever be reached with fiber.

This emphasis on AT&T Web Air needs to be constructive for the cell tower REITs as a result of it represents AT&T trying to take market share away from the everyday web service suppliers. It ends in extra demand for cell towers by shifting extra residence web connections to run on cell towers.

Why Would Analysts Care About EchoStar?

In principle, EchoStar would possibly cut back the quantity of tower property they lease if they’re going to run extra of their service by means of AT&T’s community. The settlement to make the most of AT&T’s community was a part of the deal that resulted in AT&T agreeing to pay $23 billion. It might not have been a big half, but it surely was a consideration (per administration’s commentary):

Sure, the brief reply is that we finally count on there will be incremental worth that is generated from the Increase relationship shifting ahead, and that is a part of the contribution as to why we expect this has been a superb transfer for us. It is a full package deal and we view this as a full package deal, and so they all work collectively.

The Core Issue

The downgrade for SBAC actually doesn’t look like pushed by this explicit occasion.

There is a problem from worldwide churn, however that’s been a identified issue for fairly some time.

SBAC doesn’t have information facilities (like (AMT)) and doesn’t have a structural transformation (like (CCI) eliminating fiber). However these aren’t new surprises.

Enable me to paraphrase the remaining argument towards SBAC:

SBAC’s value rallied year-to-date due to improved expectations for home leasing. These expectations had been primarily based on administration elevating steering and speaking about a rise in service software volumes.

The bears look like doubting administration’s steering. I’m not.

What Did SBAC’s Administration Say?

I pulled up our Q2 2025 SBAC Replace as a result of I knew it might have probably the most pertinent data. Right here’s the quote:

SBAC

Effectively, it positive seems to be like SBAC was speaking about leases that had been signed. These are contracts. It isn’t simply carriers inquiring about potential leases. It’s signed contracts.

However What if AT&T Reduces New Contracts?

SBAC has an association with AT&T to ascertain minimal volumes for leases. However SBAC would at all times prefer to signal leases for greater than the minimal quantity of areas.

What if this deal causes AT&T to signal fewer leases over the following a number of years?

Is that theoretically potential? Certain. However it’s the other of administration’s commentary about deploying the mid-band spectrum “as quickly as potential” and deploying the low-band spectrum “inside the multi-year capital funding steering supplied with its second quarter 2025 earnings launch.”

I wasn’t capable of finding a single remark from AT&T suggesting they had been reducing again on plans to deploy spectrum. As a substitute, I discovered this quote:

The acquired licenses will enable AT&T to proceed to be a pacesetter in wi-fi by means of enhanced 5G protection, even better reliability and sooner speeds.

Have been they going to attain better reliability and sooner speeds by shopping for spectrum and never deploying it?

On the decision with buyers, AT&T’s CFO stated:

Particularly, we count on it is going to drive incremental service income and EBITDA inside the first 24 months following deal shut, with accretion to adjusted EPS and free money circulate anticipated in yr 3, when the anticipated progress in EBITDA will greater than offset the incremental curiosity expense and capital investments that we’ll incur because of the transaction.

That was a part of his ready remarks. He’s very particularly speaking about rising service income and EBITDA to greater than offset the curiosity expense. Have been they going to develop service income and EBITDA by squatting on the spectrum?

Conclusion

I don’t see an enormous unfavorable for SBAC right here. AT&T didn’t signal an enormous leasing settlement for satellites. They bought an enormous quantity of spectrum. They need to use that spectrum to increase their AT&T Web Air section. That doesn’t cut back their want for towers. It transitions much more of the marketplace for “residence Web” to going by means of cell towers. I preserve a Robust Purchase outlook on SBAC.